For more than a century, the United States’ influence in Latin America and the Caribbean (LAC) stood as an unquestioned cornerstone of international politics. However, China’s entry into the World Trade Organization (WTO) in 2001 marked the start of a quiet yet profound transformation that is reshaping the region’s geopolitical landscape. This shift does not represent a simple succession of hegemonies, but rather a complex process of reconfiguration in which geopolitics and geoeconomics intersect, producing a more complex and dynamic geopolitical board.

The evidence of this transformation is overwhelming. In just two decades, China has evolved from a marginal actor to South America’s principal trading partner since 2010, and the second largest in the broader Latin American region—projected to surpass the United States by 2035. This meteoric rise is underpinned by a multifaceted and far-reaching strategy, in contrast to what many analysts view as strategic neglect on the part of Washington.

Trade as the Driving Force

Trade volume offers the clearest indication of this structural transformation. Trade between China and LAC has experienced exponential growth: from a modest $ 12 billion in 2000, it surged to $450 billion in 2023 and reached a historic high of $ 518 billion in 2024.

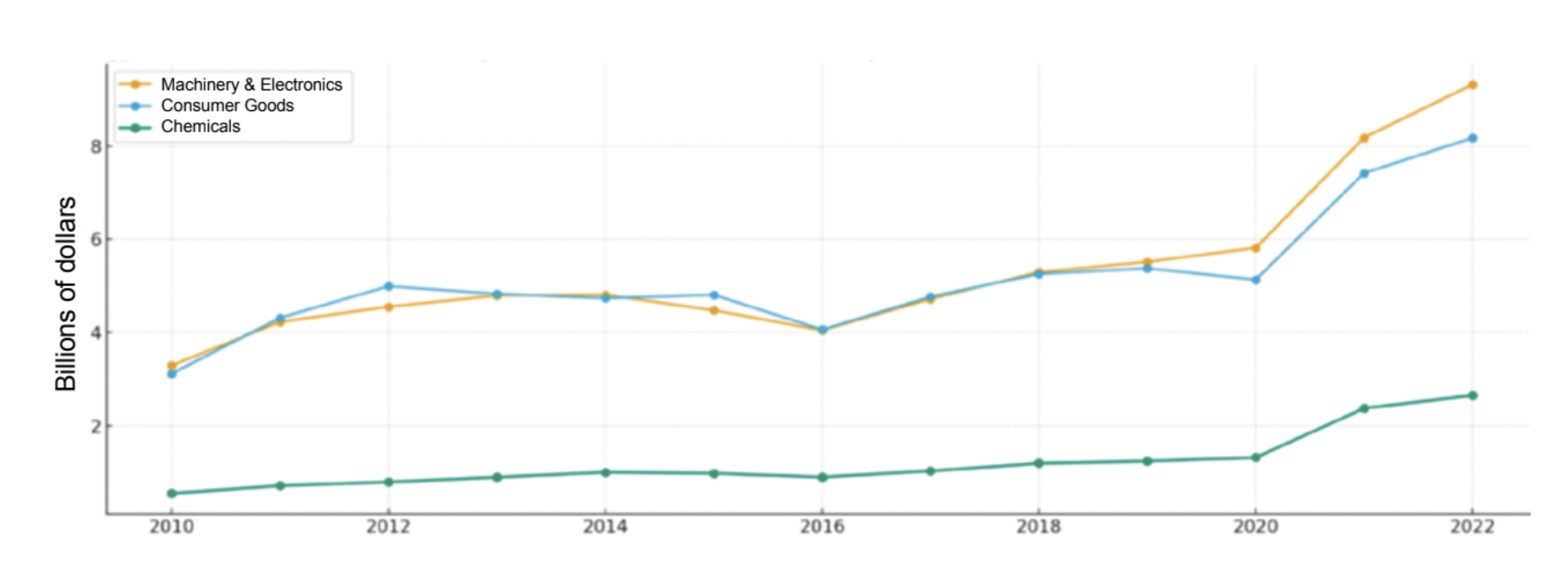

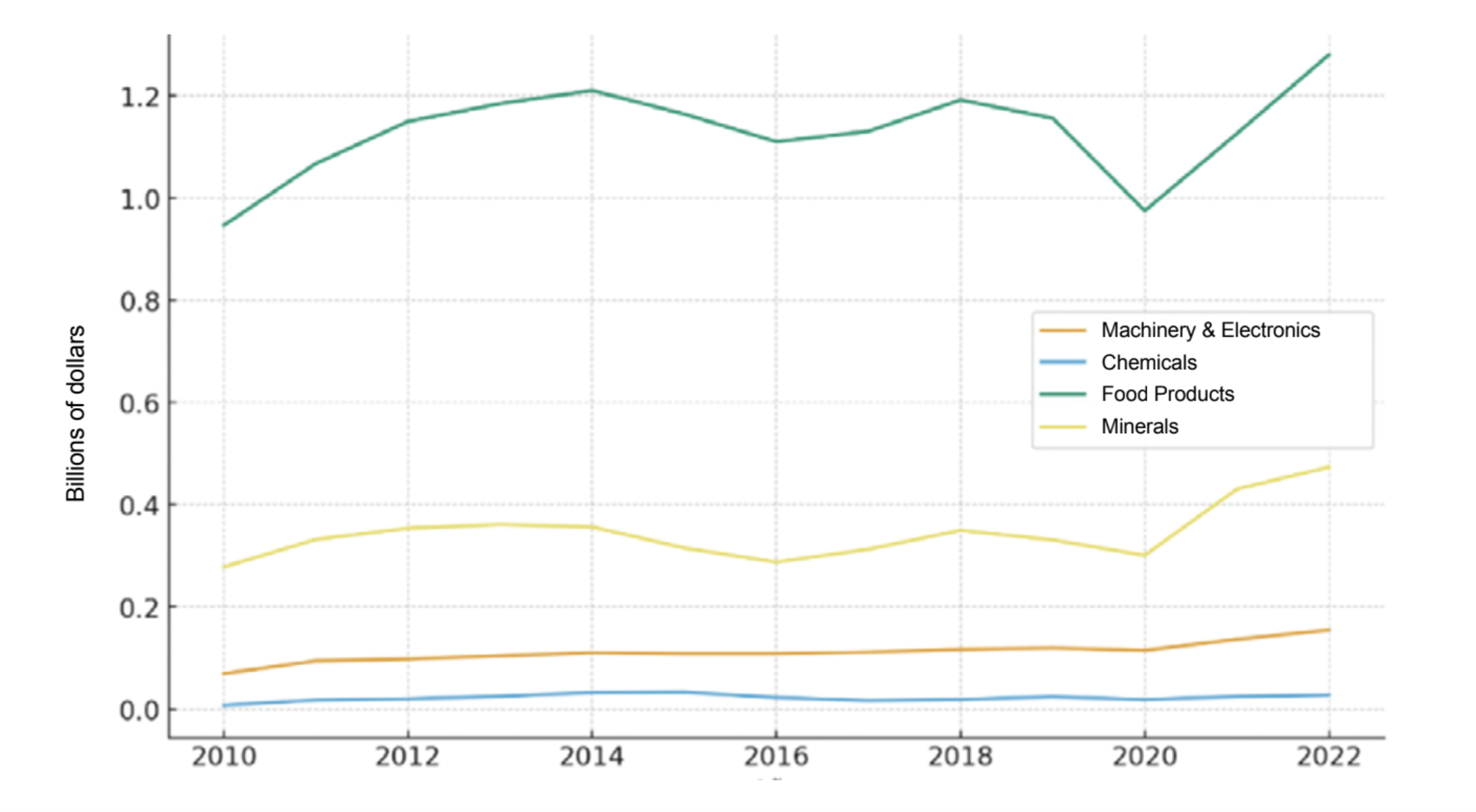

This rapid growth reflects a highly complementary, yet potentially problematic, relationship. Latin America primarily exports raw materials—with five products accounting for 67.2% of total exports: copper, soybeans, iron ore, crude oil, and refined copper—while importing high-value manufactured goods such as electrical machinery, mechanical equipment, and vehicles (see Figures 1 and 2).

This trade pattern has generated substantial surpluses for commodity-exporting countries such as Brazil and Chile, where surpluses often exceed 2% of GDP, but it has exacerbated structural deficits in more industrialized economies like Mexico, which recorded nearly -6% of GDP in 2023.

Trade between the United States and LAC, in turn, reflects a structural pattern that highlights both the priorities and vulnerabilities of the two parties. Over the past decade, trade has grown in absolute terms, but its underlying structure has remained unchanged: the United States primarily exports high value-added industrial goods—machinery, electrical equipment, and manufactured products—while importing natural resources, energy, and food from the region (see Figure 3). This trade structure underscores LAC’s significance as a strategic supplier of raw materials essential to U.S. energy and food security, while simultaneously revealing Latin American countries’ reliance on international markets to sustain their export‑oriented economies.

Nevertheless, what matters is not only the volume of trade, but also the geopolitical competition embedded within it. While U.S. trade with Latin America has grown, its relative weight has declined in the face of China’s rise —a rise driven not only by its demand for natural resources but also by its expanding presence in manufacturing and finance.

The paradox is striking: despite sustaining substantial trade with LAC, the United States has been unable to convert this economic presence into renewed strategic influence. China, by contrast, has moved more assertively to seize emerging opportunities, positioning itself as a strategic counterweight to Washington’s long-standing centrality in the region.

The United States’ trade relationship with the region is marked by its maturity and structural stability, whereas China’s is more recent and rapidly expanding. Washington primarily exports capital goods, advanced machinery, and industrial components, many of which feed into regional value chains, particularly in Mexico and Central America under the USMCA framework. This creates a productive interdependence that goes beyond simple exchange.

Import Patterns: Diversification vs. Primary Concentration

When it comes to imports, both countries acquire commodities, though with distinct areas of emphasis. The United States maintains a diversified import profile from LAC—energy, strategic minerals, agro-industrial products, and basic manufactured goods—aligned with its energy and food security priorities. China, by contrast, focuses on large-scale imports of primary resources – soybeans from Brazil and Argentina, copper from Chile and Peru, and oil from Venezuela and Brazil—which are essential for sustaining its industrial and urban growth. Such concentrated demand exerts an immediate and significant impact on international commodity prices and reshapes production incentives across the region.

The outcome is a segmented regional trade pattern, in which China’s economic complementarity reinforces primary-export growth, whereas the relationship with the United States remains important but its relative share in regional trade declines. While the United States maintains a more integrated and diversified trade portfolio, China operates as a concentrated engine of demand, capable of reshaping Latin America’s export structure and expanding its influence over the region’s economic and political agenda.

The Evolution of Investments: from State Loans to Strategic Sectors

China’s strategy in the region extends well beyond trade and is particularly evident in its investment footprint. Although Chinese FDI accounted for only 2% of total inflows in 2024, according to ECLAC, this figure significantly understates its real impact. Much of China’s investment is routed through third countries or recorded as concessions and construction contracts, thereby falling outside conventional FDI classifications. The real stock of Chinese investment reveals a different picture: it grew from $126.3 billion in 2015 to over $600 billion in 2023.

The qualitative evolution of China’s investment strategy is evident in its shift from predominantly large state loans to direct investments in new plants operated by companies in high value-added sectors. Companies such as BYD and Great Wall Motors are establishing electric vehicle plants in Brazil and Mexico; Huawei is deploying 5G infrastructure across the region; and investments in critical minerals, including lithium in the Lithium Triangle and copper in Peru, are rapidly increasing. Geographically, these investments are concentrated in the largest economies: Brazil (34% of the total between 2020 and 2023), Argentina (22.5%), Mexico (15%), and Peru (11%).

The Paradox of the Largest Investor Losing Influence

As China diversifies and deepens its investment presence in the region, the United States faces a unique paradox. In 2024, Washington remained the main foreign investor in the region, accounting for 38% of total investment, equivalent to $188.962 billion. However, this leadership position has coincided with a relative decline in influence, particularly in South America, where China has steadily expanded its presence. This contradiction—holding the position of largest investor yet losing strategic centrality— reflects dynamics that extend well beyond economics.

On the commercial front, the United States retains its historical strengths, yet it now faces growing competition from China. Although the United States was long regarded as the region’s natural strategic partner, Beijing has surpassed Washington as the leading trading partner in countries such as Brazil, Chile, and Peru, and is now the second largest in Mexico. North American trade policies — often associated with the America First doctrine and perceived as aggressive due to tariff measures — have encouraged Latin American producers to redirect their attention toward Asian markets. As a result, numerous governments and economic sectors in LAC perceive that Washington has deprioritized the region.

Chinese Agility vs. U.S. Standards

The differences in operational frameworks are also significant. While Chinese companies tend to operate faster and with fewer political, environmental, or labor constraints, U.S. companies face stricter standards for transparency and sustainability. Although these requirements contribute positively to governance, they can also reduce the relative competitiveness of U.S. companies when compared with their Chinese counterparts.

In this context, U.S. investment is increasingly directed toward strategic sectors connected to national security priorities and the restructuring of global supply chains. Notable examples include projects in Mexico and Costa Rica aimed at strengthening the semiconductor supply chain, as well as initiatives in Brazil designed to advance critical mining operations under environmentally responsible extraction standards.

Flagship Projects: The Geopolitics of Cement and Steel

The competition between China and the United States is increasingly visible in infrastructure projects that are transforming the region’s economic landscape. The port of Chancay in Peru, developed by cosco with an investment of $3.5 billion, represents far more than a conventional port facility: it constitutes a strategic hub that will shorten shipping times to Shanghai by ten days, intentionally bypassing the Panama Canal. The project generates economic dependencies, expands influence, and provides a tangible logistical advantage that disrupts established trade flows.

The Central Bioceanic Corridor, in turn, illustrates China’s broader ambition to reconfigure South America’s logistical landscape. By establishing an efficient terrestrial route for Brazilian raw materials to access the pacific, the project disrupts long-standing Atlantic-oriented trade flows and deepens South America’s economic ties with Asia, further sidelining routes that have traditionally benefited the United States and Europe.

For more than a century, the Panama Canal has stood as a quintessential symbol of American power and engineering prowess. Today, however, it faces indirect competition from the new trade routes promoted by China. Chancay and the Bioceanic Corridor form part of a calculated strategy to dodge the Panama Canal thereby diluting its geoeconomic monopoly and reducing strategic dependence on a route historically controlled by one of Washington’s closest allies.

Financing, Debt and Internationalization of the Yuan

In terms of financing, debt, and the internationalization of the yuan, Chinese policy banks have extended loans exceeding $120 billion since 2005, with some estimates reaching upwards of $141 billion. The primary recipients of these loans were Venezuela, with approximately $60 billion, and Brazil, with $31 billion.

Although loans from Chinese policy banks have dropped sharply in recent years—falling to nearly zero for Belt and Road Initiative (BRI) projects in 2020, with only a slow post-pandemic recovery—they were instrumental in enabling China to expand its influence in the region through infrastructure diplomacy. Factors contributing to this decline include diminished demand for Chinese financing in LAC, changes in the management of China’s foreign exchange reserves, and a more cautious approach to risk by Chinese lenders.

Currently, China’s financing strategy is supported by new lines of credit. At the China-CELAC Forum held in Beijing in May 2025, Chinese President Xi Jinping announced the creation of new yuan-denominated credit lines. The total of these lines amounts to ¥66 billion, equivalent to approximately US$9.2 billion, aimed at supporting infrastructure development, poverty reduction, and digital transformation.

In addition to these credit lines, China has deepened its financial ties and advanced the internationalization of its currency, the renminbi (RMB), through the signing of currency swap agreements. By 2022, China had concluded bilateral local currency swap agreements with the central banks of Argentina, Brazil, Suriname, and Chile. These agreements seek to expand the use of the yuan in cross-border transactions. A notable example of such agreements is the one signed by China and Brazil in February 2023. The two countries agreed to a currency swap worth R$157 billion (approximately US$28 billion), set to remain in effect for five years.

The U.S. Response: Limited Initiatives and Structural Challenges

President Joe Biden—who, as vice president, had already advocated for revitalizing U.S. influence in the region to offset China’s growing presence—framed China as a strategic rival and committed to reinforcing partnerships in the Western Hemisphere. In 2021, working alongside G7 partners, the administration launched the Build Back Better World (B3W) initiative as an alternative to China’s Belt and Road Initiative (BRI), aiming to finance infrastructure projects in low- and middle-income countries, including those in Latin America. However, its initial impact was largely symbolic: only $6 million was committed in the first year—a negligible amount compared to the hundreds of billions mobilized by Beijing. The initiative was later rebranded as the Partnership for Global Infrastructure and Investment.

At the 2022 Summit of the Americas, President Biden announced the launch of the Americas Partnership for Economic Prosperity, an initiative aimed at enhancing regional economic competitiveness. At the same time, legislative proposals such as the Western Hemisphere Nearshoring Act (H.R. 772) were introduced in the 118th Congress to establish permanent trade partnerships and encourage the reshoring or nearshoring of supply chains from China to countries closer to the United States. Yet, these initiatives have stalled in Congress, underscoring internal limitations and the absence of political consensus around a more ambitious strategy supported by adequate resources.

The DFC Paradox: Investment Without Reach

One of Washington’s primary instruments is the U.S. International Development Finance Corporation (DFC), which oversees financing for projects abroad. One example often cited as a success is the approval of $30 million for a cobalt and nickel mining project in Brazil, intended to support the production of lithium-ion batteries. Yet this example remains an exception. Under its current mandate, the DFC considers every Latin American nation, apart from Bolivia, Honduras, Nicaragua, and Haiti, too wealthy to qualify for most of its funding programs. The Brazilian project secured approval only after an extraordinary multi-agency review.

This structural limitation creates a gap that China has been quick to exploit. Guyana offers a telling example: despite being a strategic partner where U.S. companies like ExxonMobil and Hess extract vast oil reserves, the country was denied DFC financing for an oil port expansion due to its newly acquired oil wealth. This rejection paved the way for Chinese contractors to undertake critical infrastructure projects. As Ryan Berg of the Center for Strategic and International Studies observes: “The United States extracts the oil, while China builds much of the infrastructure.” This paradox highlights the disconnect between Washington’s strategic rhetoric and the reality of its foreign policy tools, which are often inflexible, resource-constrained, and unable to match China’s combination of no-strings-attached approach and bureaucratic agility.

This contrast (see Table 1) helps explain why the Chinese model has proven so effective in quickly gaining ground, particularly in a context where many countries face urgent infrastructure needs and demand immediate financing.

Conclusion

Studying the competition between the United States and China in Latin America and the Caribbean reveals not only the dynamics of their bilateral relationship but also broader transformation in the international system. While Washington continues to hold quantitative advantages in foreign investment and in sectors such as financial services and semiconductors, Beijing has steadily built a multifaceted presence that integrates trade, infrastructure, technological innovation, and cultural outreach.

Rather than a simple hegemonic succession, what emerges is a landscape of overlapping spheres of influence, in which each power occupies distinct niches and regional countries exercise significant agency.

In Brazil, for instance, China has become a central trading partner, while the United States remains a major investor in strategic industries. In Mexico, structural dependence on the U.S. economy coexists with China’s growing role in manufacturing. Across the Andean nations, efforts to secure financing for infrastructure and critical mining projects often involve parallel negotiations with both Washington and Beijing.

The key conclusion is that the future of Latin America and the Caribbean will depend not only on the intensity of U.S.–China competition, but also on the region’s ability to articulate its own strategy for international integration.

Such a strategy must balance the pursuit of diversification with the need to avoid new forms of dependency, while aligning economic objectives with environmental, social, and democratic governance priorities.

In this sense, Latin America and the Caribbean is not merely a passive stage for great-power rivalry, but an active player whose capacity to maneuver can help shape the rules of an evolving international order.